Understanding Scopes

You may or may not be familiar with the terminology of scopes, specifically 1, 2 & 3. These are defined in the GHG Protocol Corporate Standard and relate to the types of emissions an organisation directly or indirectly produces. These are defined as:

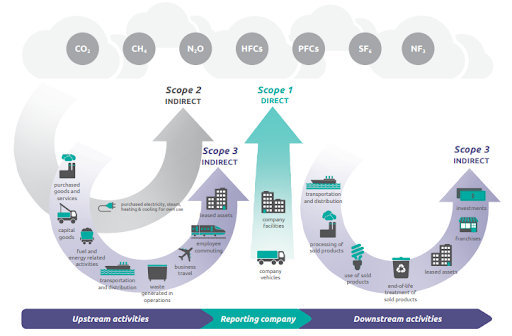

Scope 1 (Direct Emissions): Emissions from activities owned or controlled by your organisation that release emissions into the atmosphere. They are direct emissions. Examples of scope 1 emissions include emissions from combustion in owned or controlled boilers, furnaces, vehicles; and emissions from chemical production in owned or controlled process equipment.

Scope 2 (Indirect Emissions): Emissions released into the atmosphere associated with your consumption of purchased electricity, heat, steam and cooling. These are indirect emissions that are a consequence of your organisation’s activities but which occur at sources you do not own or control.

Scope 3 (Indirect Emissions): Emissions that are a consequence of your actions, which occur at sources which you do not own or control and which are not classed as scope 2 emissions. Examples of scope 3 emissions are business travel by means not owned or controlled by your organisation, waste disposal which is not owned or controlled, or purchased materials or fuels.

Compared to other industries, the energy legislation industry is still in its infancy. It has only been two decades since the EU Emissions Trading Scheme (ETS) and Climate Change Levy (CCL) was introduced. Since then, through directives like the Energy Performance of Buildings (EPBD), other legislation has come into force across the EU and the United Kingdom.

GHG emission scopes play an important role in several pieces of legislation and all of this legislation currently only targets quoted companies, large unquoted companies (including charitable companies) and large Limited Liability Partnerships (LLP) who are legally required to report scopes 1 and 2. For most, Scope 2 is the most relevant and at present there is no formal requirement to report on Scope 3 emissions. However, Scope 3 can account for around 80-90% of an organisation’s emissions.

Further to this, there is no legal requirement for SMEs to report on their energy consumption or emissions. However, the Department for Business, Energy & Industrial Strategy (BEIS) is drafting legislation that will implement a new Small Business Energy Efficiency policy mechanism and another that will introduce a new minimum energy efficiency standards for rented business properties that are due in the next 12 to 18 months. Their definition of what an SME is yet to be determined but to match the requirements of Streamlined Energy & Carbon Reporting (SECR), they are likely to use the Companies Act for reference.

Businesses should have strategies and measures in place that identify their current operational energy profile, even if this is a simple monitoring of monthly site consumption and costs but this can also include GHG emissions. Once an assessment has been made, then a full audit to identify opportunities that can be implemented should be conducted. Within this, financial paybacks should be included.

It should be made clear that once carbon and energy consumption has been reduced as much as possible within a business’s operations, something that should be reviewed annually, then is the time to look into carbon offsetting projects.

If you are starting out in this journey and require support in completing this, 2EA offer a full Building Energy Audit service that includes:

- Data correlation of the building(s) energy usage (assumes copies of the buildings utility bills are forwarded to 2EA Consulting prior to site audit). Includes correlation of any on-site fuels and/or renewables.

- Analysis of energy consumption and calculation of significant energy use.

- Assess, quantify and benchmark significant energy consumption across site(s) and identify an appropriate baseline to measure energy performance.

- Carry out audits of building(s) and identify energy saving opportunities.

- Provision of a full audit report detailing findings, energy saving measures & strategies, cost analysis & payback period and identification of possible legislation that may offer energy saving grants.

- 2EA Consulting will provide consultancy services to clients with regards to BEA Works.